This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Maybe you missed your chance to attend FinovateFall earlier this month. Or maybe you want to watch your favorite demos over again. Either way, today’s your day. We’ve just released all of the videos from the 75 companies that demoed their fintech on stage.

All of the 7-minute demos are available to stream and download for free at Finovate.com. And if you don’t know where to begin, we’ll get you started with the nine demos that won Best of Show at the event.

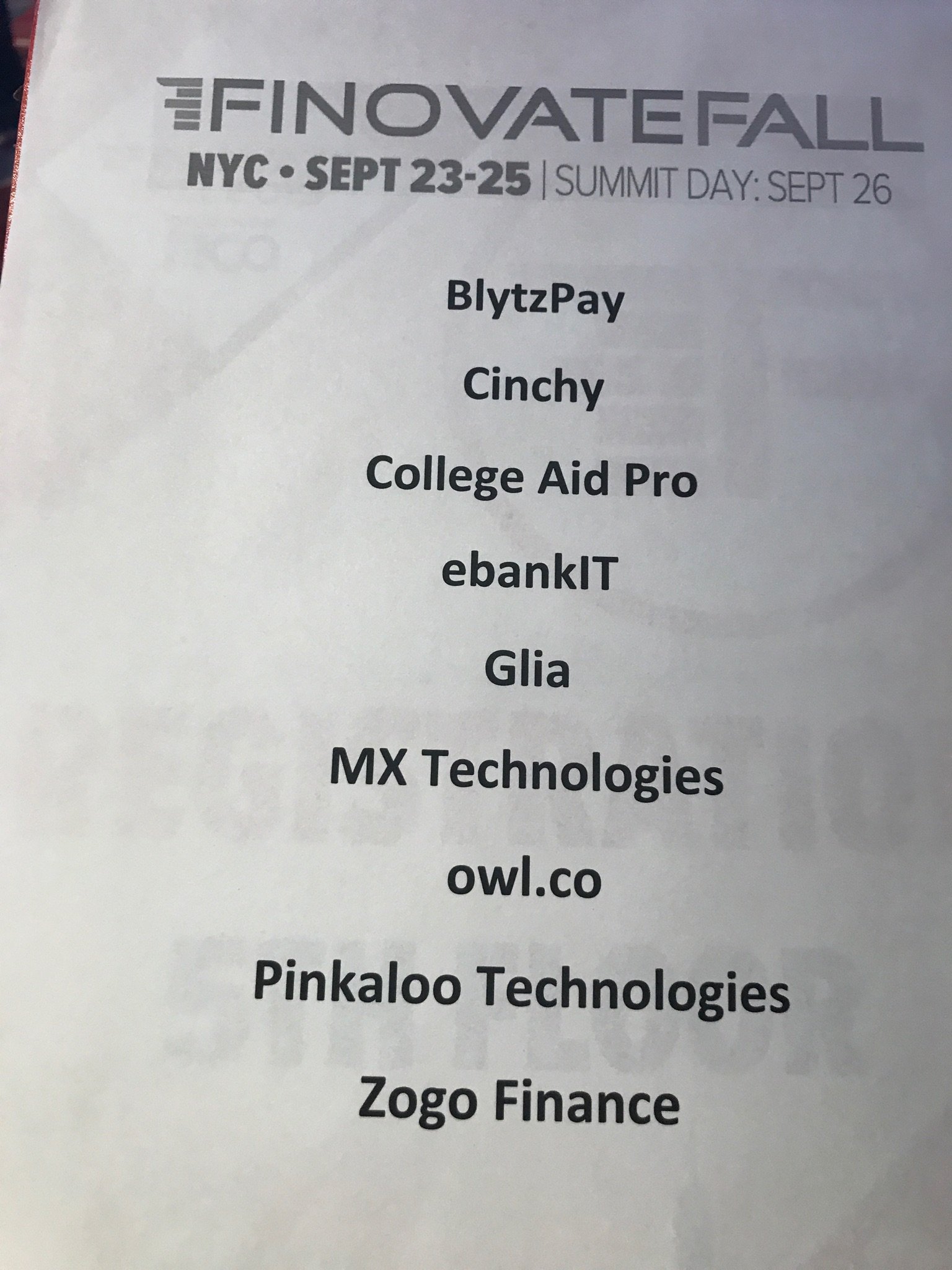

The votes have been cast and the ballots counted. And after two days of live fintech demos from 75 innovative companies, here are the best of the best: the companies our attendees have deemed FinovateFall’s Best of Show.

BlytzPay for its text-to-pay solution that makes billing and communication simple, streamlined, and secure while providing flexibility to pay by card, check, or cash. Demo video.

Cinchy for its Data Collaboration Platform that lets data work the way it should: connected, controlled, and accessible for real-time collaboration. Demo video.

College Aid Pro for its innovative technology, supported by a community of financial advisors, that changes the way America shops for college. Demo video.

ebankIT for its omnichannel digital banking platform that helps banks and credit unions transform their businesses. Demo video.

Glia for its technology that creates digital-first moments that simplify and transform communications between businesses and their customers. Demo video.

MX Technologies for its platform that helps financial institutions and fintechs quickly and easily collect, enhance, analyze, present, and act on their financial data. Demo video.

owl.co for its instant KYC/AML tool that automates enhanced due diligence on both individuals and companies. Demo video.

Pinkaloo Technologies for its solution that helps financial institutions attract and retain customers and increase deposits and fees by powering their customers’ charitable giving. Demo video.

Zogo Finance for its technology that leverages partnerships with financial institutions to reward kids for learning financial literacy. Demo video.

Those in attendance at this year’s FinovateFall can attest to the energy and enthusiasm that characterized our conference this week. Congratulations to all 75 of the companies that demonstrated their fintech innovations on stage and a heartfelt thanks to our partners, sponsors, and onsite tech team for making this year’s autumn event a smashing success.

Notes on methodology:

1. Only audience members NOT associated with demoing companies were eligible to vote. Finovate employees did not vote.

2. Attendees were encouraged to note their favorites during each day. At the end of the last demo, they chose their three favorites.

3. The exact written instructions given to attendees: “Please rate (the companies) on the basis of demo quality and potential impact of the innovation demoed.”

4. The nine companies appearing on the highest percentage of submitted ballots were named “Best of Show.”

5. Go here for a list of previous Best of Show winners through 2014. Best of Show winners from our 2015 through 2019 conferences are below:

Greg Palmer (@GregPalmer47) is Vice President of Finovate and Master of Ceremonies for FinovateFall 2019. His essay below is featured in the FinovateFall 2019 Supplement available in full here.

One of my favorite aspects of working in fintech is the way that it inadvertently reveals fundamental truths about human beings

As an industry, we have massive piles of hard data documenting human behavior, and we use that data to anticipate what people are likely to do and when they’re likely to do it. We can use this data to help reach customers with a specific message when we think they’re likely to buy a car or a home. We can use it to look for anomalies in customer behavior, which can be early warning signs of fraud. We can even use it to create a user experience that’s statistically likely to please a given user based on the demographic and personal information we have on them.

In many cases, though, this data doesn’t do much beyond proving what we’ve intuitively known (or suspected) for years. For example, the banking industry has known for a long time that people struggle to start saving as early and as often as they should, and that we’re all too lax when it comes to protecting our passwords and account information. We have data that can back this up, but the results are hardly a shock to anyone who’s paying attention. The average financial services customer, much to the annoyance of the high-achievers in the fintech space, usually doesn’t take basic steps to safeguard against fraud, optimize retirement savings, or plan appropriately for future expenses.

The fintech industry responds to this by creating products and innovations that are designed to make it easier for people to engage in responsible behavior. We’ll see this play out on stage at FinovateFall, where wealth management, savings, and security are looking like resurgent themes. I like to group these into a broader category of fintech, though, which I call “grown-up fintech”. Innovations in this larger category essentially boil down to helping end-users act more responsibly and manage aspects of their finances that they’ve ignored until now.

The real challenge with “grown-up fintech” usually has less to do with the technology itself, and more to do with getting people to change their habits. For most users, it takes some sort of shock or anomaly to spur a behavior change. The irony, of course, is that by the time this sort of shift occurs, it’s usually too late. Creating and sticking to a budget is far more valuable if you do it before you’re deep in credit card debt; talking with your parents about their end-of-life plans and their finances is much more fruitful while they’re still vibrant and healthy; and adding security features like two-factor-authentication (or even simply updating your password routinely) is way more effective before you get hacked.

(I don’t mean to imply that these shocks are always negative, either. Positive life events such as getting married, having children, or buying a house all come with unusual financial implications, and it’s way easier to navigate those shifts if you prepare for them ahead of time.)

If you sit in the audience at Finovate, you’ll be surrounded by people who know all of this. They will nod knowingly as presenters on stage talk about banking customers as though they were children who simply can’t be trusted to do their homework when the adults are out of the room.

I don’t have a problem with this at all, for the record. It’s not meant to be malicious (it’s usually coming from more of a parental, protecting place) and it’s not incorrect. After all, we have the data to back it up. What interests me, though, is how those same people who so easily see and understand this behavior in their customers struggle to account for it inside their own organizations. If we continue the parental analogy here, we have a lot of people falling into the classical parenting misstep of “do as I say, not as I do”.

When it comes to financial systems, there are a variety of major threats to the status quo. New, disruptive players entering the financial services space, tech giants launching competing financial products, more frequent (and more powerful) cyberattacks, and the increasing specter of a recession are just a handful of the major ones. On the flip side, new opportunities abound for those who are able to take them – new customer-bases are opening up, new sales and marketing technologies make it easier to access them, and back-end improvements allow for increased efficiency and lower overhead.

Many forward-thinking financial institutions are protecting themselves against those threats and setting themselves up to reap the rewards of those new opportunities. But an alarming number of FIs are falling into the same trap that too many of their customers are: they aren’t making the “responsible” or “grown up” decisions right now that will make their lives easier in the future. Instead, they are waiting for the next big shock to force them to change their behavior.

In reality, this behavior isn’t childlike – it’s human. And it’s something that we’re all guilty of to some extent. Equally “human” is the tendency to recognize behavior in others that we fail to see in ourselves. The financial industry generally, and fintech specifically, puts people in a unique position to see and understand these basic human behaviors, which creates a powerful opportunity for learning and growth. Those that see this behavior, learn from it, and apply those lessons internally will be better prepared for the inevitable shocks to the system that the future will bring. Those that don’t will be left wishing they’d done more.

The time to start budgeting is before you’re deep in debt; the time to secure your accounts is before you get hacked; the time to discuss your parents’ finances is before their health starts to fail; and the time to future-proof your bank is before the next shock to the system hits.

While you’re busy scheduling meetings and crafting your schedule for FinovateFall, 75 companies are busy rehearsing their seven minute demos. But don’t worry – if you’ve been procrastinating and still haven’t registered, there is still time to do so either on our event page or at the registration desk on Monday.

In need of last minute details? We’ve got you covered.

Where

The New York Marriott Marquis hotel at 1535 Broadway, New York, NY 10036.

Registration opens at 8:00 am on Monday, September 23. The first demo session begins at 9:00 am sharp so be sure to arrive early, grab a cup of coffee, and settle into a seat.

Be sure to stick around for the Summit day that will take place after FinovateFall. On Thursday, September 26, we’ll take a deep dive into the topics of AI, wealthtech, and investech. It’s simple to add the Summit day onto your existing ticket – just visit the registration desk for more details.

Awards

Speaking of bonus content, the first-ever Finovate Awards ceremony will take place Tuesday evening, September 24, at New York’s Edison Ballroom. We’ve curated a list of nominees for a range of awards and will be revealing and celebrating the winners with a night of champagne, good humor, and great food.

Best of Show

The Finovate Awards event is separate from Finovate’s Best of Show awards, which will be announced at the end of the last demo session on Tuesday. Attendees may cast their vote for the best demo at FinovateFall using the Brella app. Simply download the Brella.io app from the Apple App store or Google Play to get started. You can find the event code on the back of your name badge.

We’ll see you at the event! If you have additional questions, please visit our contact page and reach out one of our representatives.

In this sponsored blog post, Akshatha Kamath, Content Marketing at MoEngage, breaks down new privacy legislation which could impact financial institutions across the states.

Stronger

privacy protection and greater data transparency online are growing global

trends. The Cambridge Analytica scandal, in which the Facebook data of at least

87 million people were misappropriated, and other instances like this have

brought attention to how businesses collect, use, and sell consumer data.

Concern over the use and misuse of this data is widespread.

In many global jurisdictions, the response has been privacy legislation which forces businesses to comply with sometimes onerous regulations regarding consumer data and privacy. One of these pieces of legislation is the California Consumer Privacy Act. In its second section it lays out how pervasive privacy concerns have become and how “it is almost impossible to apply for a job, raise a child, drive a car, or make an appointment without sharing personal information.”

All of this data can be great for marketers, but businesses need to comply with privacy laws in order to avoid fines and stay up to date with consumer demand for privacy and data transparency online.

The California Consumer Privacy Act (AB-375)

The

California Consumer Privacy Act of 2018 (CCPA) is by far the strongest privacy

legislation enacted in the United States at this time. Businesses must be in

compliance by January 1, 2020 (the starting date on which the state can bring enforcement actions involving

noncompliance).

For marketers there are three major things to be aware of. First is that wherever personal information is collected businesses must disclose what information they collect and how they will use it. Secondly, businesses have to provide consumers with the ability to “opt out” of having their information sold to third parties. Thirdly, businesses must allow consumers to view and delete the information that has been collected about them.

Is My Company Affected by the CCPA?

If

your business (or for-profit entity) is located in California and meets any of the

following criteria, it has privacy requirements that need to be met under the

law. The criteria are:

Your business’ annual revenue is

over $25 million

Your business receives information

of over 50,000 consumers, households, or devices annually

At least half of your business’

annual revenue comes from selling personal information

The law doesn’t differentiate between brick-and-mortar and online companies. This means that even a company with no physical presence or employees in California could still do business there and therefore has obligations under the law. So your business doesn’t even need to be located in California for the California Consumer Privacy Act to apply to you. Like the GDPR, CCPA will affect businesses outside the law’s jurisdiction.

Consumer’s Rights Under the CCPA

Consumers have new rights under the CCPA that companies need to be aware of. These rights fall into three broad categories:

The Right to Knowledge – Under the CCPA, businesses must allow consumers to obtain, twice per annum at zero cost, all the information that the business has about them, how that information was collected, and who else has been given said information.

The Right to be Forgotten – The CCPA stipulates that consumers must be able to request the deletion of all of their personal information from a company. If the information has been shared with third parties then those parties must also delete said information.

The Right to Control who has Access to their Information -Businesses must allow consumers to be able to opt out of the resale of their information. Consumers under the age of 16 must affirmatively opt in to allow the resale of their data. Consumers under the age of 13 must have written permission from a parent or guardian in order to allow the resale of their data.

What Marketers Need to Do

First of all, marketers need to review their current procedures and understand their policies and procedures regarding the collection, storage and use of subscribers’ data and mailing preferences. They need to know how a user’s preferences about their data can be stored and how documentation would be provided if a user requests it.

Second of all, marketers need to think in the long term about how they set up their systems. For example, even though GDPR only applies to EU visitors, many companies have opted to implement the same higher standards across their entire platform in order to proactively prepare for similar legislations. In the same vein, marketers who prepare for the CCPA will have a leg up if privacy bills that are making their way through the legislature pass in New York, Mississippi, and Massachusetts.

Penalties for Non-Compliance of the CCPA

If,

because of a business’ negligence, a consumer’s information is improperly

disclosed, the CCPA makes it easier for consumers to sue (even if there is no

evidence that the data breach caused the consumer harm!).

What

could be very costly for businesses is the potential for class-action lawsuits

due to a data breach. Companies could be on the hook for between $100 and $750

per incident (or even more if the actual damages exceed $750).

Conclusion

The

California Consumer Privacy Act will go into effect on January 1, 2020.

Marketers should prepare in advance to make changes to comply with the

regulations. At the same time, CCPA presents marketers with an opportunity to

strengthen the relationship between consumers and your business. Educate

consumers on the data you are collecting and how you make use of it. Be sure to

tell them their rights under the CCPA and how you are compliant. This can build

trust with consumers and help you use the CCPA to your advantage.

A look at the companies demoing live at FinovateFall on September 23 through 25, 2019 in New York City. Register today and save your spot.

UBDI (short for Universal Basic Data Income) is reinventing financial and market research by empowering individuals to monetize aggregated, anonymized insights from their data.

Features

Provides aggregated, anonymized historical and real-time data points combined with qualitative data from paid users

Reaches the perfect audience with PrivateMatch Technology

Represents the gold standard of GDPR/CCPA compliance

Why it’s great Data and privacy can work together for richer insights when you empower the individual with their own data.

Presenters

Dana Budzyn, CEO and Co-Founder Budzyn is an engineer and published researcher with NASA for her work in Optics and Photonics technology. Watch her TEDx “Owning Your Digital Self: Monetizing Your Personal Data.” LinkedIn

Shane Green, Executive Chair and Co-Founder In addition to being Founder/Chair of UBDI, Green is also the U.S. CEO of personal data platform digi.me (following the merger with Personal in 2017 where he was founder/CEO). Green also founded The Map Network, which was acquired by Nokia/NAVTEQ. LinkedIn.

A look at the companies demoing live at FinovateFall on September 23 through 25, 2019 in New York City. Register today and save your spot.

Buckzy is an enabler of banks and financial institutions. The company is fundamentally transforming the way people move money around the world with its real-time cross-border payments ecosystem.

Features

Real-time cross-border payments ecosystem

Availability 365 days a year

24/7 access even inside of traditional banking hours and holidays

Why it’s great Cross-border P2P payments, bill payments, global trade payments, and international student payments can now be settled in real-time with 365 days, 24×7 accessibility to funds.

Presenter

Lindsay Mulligan, Global Chief Marketing Officer Mulligan is a global marketer, innovator, and digital martech strategist with over 12 years of experience in marketing multinational brands on a global scale for both B2B and B2C initiatives. LinkedIn

A look at the companies demoing live at FinovateFall on September 23 through 25, 2019 in New York City. Register today and save your spot.

LoanPay from CheckAlt enables financial institutions to accept check, eCheck, and card payments for various loans such as consumer loans, auto loans, mortgages, HELOCs, and credit cards.

Features

Financial institution core agnostic

Fully mobile responsive for consumers

Provides omnichannel experience for consumers and back office

Why it’s great LoanPay enables financial institutions to accept payments across all channels including in-person, through a call center, and online, for all loan types.

Presenters

Bobby Rahmanian, Chief Product and Innovation Officer Rahmanian brings more than 23 years of experience in product, payments, business operations, and technology to CheckAlt. He is spearheading the transformation of LoanPay. LinkedIn

Stacey Bryant, Senior Executive, Credit Unions Bryant brings 15-plus years of operational oversight and business development expertise in the credit union industry to CheckAlt. LinkedIn

A look at the companies demoing live at FinovateFall on September 23 through 25, 2019 in New York City. Register today and save your spot.

myGini is a customizable, AI-powered, plug-and-play card loyalty and customer engagement solution for financial institutions and retailers to drive incremental volume and sales.

Features

Digital and customizable customer engagement with each card transaction

Ability to create unique and segmented promotions

Point redemption and cash back in real time

Why it’s great myGini is a financial app that brings tangible benefits and interacts with the consumer at the right time.

Presenter

Mehmet Sezgin, Founder and CEO Sezgin is former Global Head of Payments at BBVA and former CEO and founder of Garanti Payments. He has served as a board member for MasterCard Europe for 14 years. LinkedIn

A look at the companies demoing live at FinovateFall on September 23 through 25, 2019 in New York City. Register today and save your spot.

MX is the leading data platform for banks, credit unions, and fintechs, empowering customers to easily collect, enhance, analyze, present, and act on financial data.

Features

MX Enabled is a centralized data platform that rapidly integrates amazing fintech companies to thousands of banks and credit unions creating faster time to market and reduced costs.

Why it’s great MX Enabled connects fintechs and financial institutions to a world of innovation through enhanced data.

Presenters

Brandon DeWitt, CTOand Co-Founder DeWitt is the co-Founder and CTO of MX. Prior to MX, he co-founded MyJibe, a personal financial management company, acquired by MX in 2012. DeWitt formerly worked at Baker Hill and Experian. LinkedIn.

Cosme Salazar, Product General Manager Salazar is a Product General Manager over APIs and the MX Enabled platform. He has worked in product management for over ten years including time at Instructure and Amazon. LinkedIn.

A look at the companies demoing live at FinovateFall on September 23 through 25, 2019 in New York City. Register today and save your spot.

Mylife is the leading provider of consumer reputation data including the new consumer reputation score.

Features

Assesses publicly available data to score consumer character

Enables consumers to take action to improve their score

Establishes trust in others based on their score

Why it’s great The consumer reputation score is new and being rolled out widely to enable trust and safety in online interactions between consumers

Presenters

Mark Kapczynski, SVP, Partnerships Kapczynski is the former VP of strategy at Experian and head of strategy for Yodlee’s data and analytics business. LinkedIn

Tim Peters, VP, Partnerships Peters is the former head of digital acquisition at Experian for FreeCreditReport.com along with several additional fintech companies. LinkedIn